Bottleneck Accounting

Summary

Bottleneck accounting is a managerial accounting tool which helps you to determine:

- the bottlenecks of an organization which constrain sales and revenues and;

- how much money was lost because of each bottleneck.

Bottlenecks

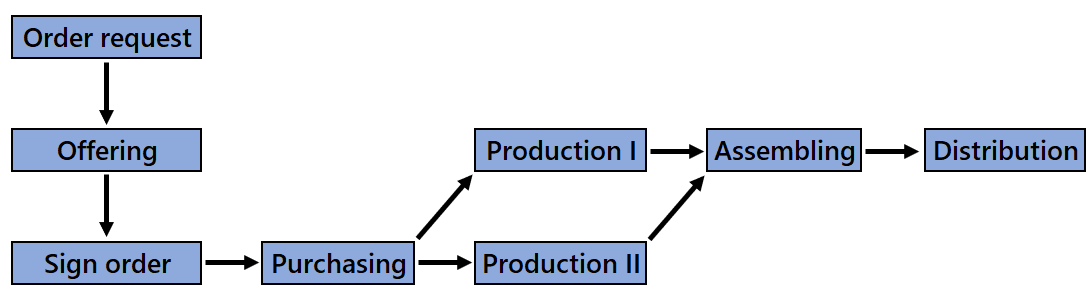

A company usually has several stages involved in the production and selling of a product or service. For example:

In practice, bottlenecks will usually arise to constrain the amount of products the firm can deliver (Kaplan and Atkinson, pp. 62). A bottleneck is the capacity constraining stage governing the output of the entire process (Slack et al, 2010). Various authors emphasize that in order to improve the output of the total production process bottlenecks in the production process must be found and managed. Schmenner and Swink (1998) cite the Law of Bottlenecks that states that the productivity of a production process is improved by eliminating or by better managing its bottlenecks. The purely practitioner-oriented work of Goldratt (1984) also emphasises that a company must concentrate on its bottlenecks in the production process in order to improve the overall performance.

Existing bottleneck detection methods

In recent years many methods that can be used to search for bottlenecks have been presented in the literature, for example:

- methods that detect bottlenecks based upon queue length (Lawrence and Buss, 1994 and Pollett, 2000);

- methods that detect bottlenecks based on the maximal production capacity of production factors (Dantzig, 1965);

- methods that detect bottlenecks based on the utilization of production factors (Krajewski et al, 2010 and Cachon & Terwiesch, 2009);

- methods that detect bottlenecks based on the active and inactive periods of machines (Roser et al, 2001);

- methods that detect bottlenecks based on the time a machine is inactive because it is waiting for the arrival of parts, a period called “starvation”, or for their removal, a period called “blockage” (Ching et al, 2008 and Li et al, 2009).

These methods focus on the factory floor and do not analyze the whole production or service delivery process, which starts with an initial stage – such as a potential client requesting a quotation – and ultimately ends with a final stage such as distribution. Because of this limited view, a bottleneck, which actually limits sales and profit but which occurs before or after the manufacturing stage, might be missed, costing the company time and money looking for a bottleneck in the wrong places.

The negative effect that a bottleneck has on profit demonstrates the urgent need to eliminate the bottleneck. Therefore, a bottleneck with less impact on profit should be given a lower priority than a bottleneck that has a drastic effect on profit. In order to determine the priority of a bottleneck, a company should determine what effect a bottleneck has on profit. However, the existing methods which detect bottlenecks by measuring queue lengths, active periods, inactive periods, periods of blockage or periods of starvation do not calculate the effect a bottleneck has on profit (Veltman, 2011).

The bottleneck accounting method

Bottleneck accounting is a suitable method to determine bottlenecks and their effect on profit, regardless of the stage in which these bottlenecks occur. The bottleneck accounting method detects the bottlenecks based on the input and output of each stage in the total production or service delivery process and the initial inventories of work in progress. It can therefore analyze all stages of the total process and thus detect the bottleneck that actually limits sales and profit.

The bottleneck accounting method also calculates the effect a bottleneck has on revenue. In this analysis, the output of the bottleneck during a given period is compared with the output of the process exhibiting the second-lowest throughput. The outputs of these processes are expressed in a common unit of measurement to ensure methodological comparability. The resulting difference between the two outputs quantifies the volume or revenue lost as a direct consequence of the bottleneck. For instance:

This differential also serves as an indicator of the urgency with which the identified bottleneck should be addressed. As a result, the bottleneck accounting method enables companies to focus on solving the most urgent bottlenecks (see also Veltman et al, 2014).

Advantages and Disadvantages of Bottleneck Accounting

The advantage of bottleneck accounting is focus. It reports which stage in the production-and-sales process limits an organization’s output, sales and profit, and so enables managers to concentrate specifically on the stage that constrains sales volume and revenue. A further advantage is that it establishes the priority of the management actions required, by quantifying how much sales volume and revenue are lost because of each bottleneck. Bottleneck accounting thus makes it possible to estimate how much performance would improve if a bottleneck were eliminated, assuming all other conditions remain unchanged.

Bottleneck accounting also has a number of disadvantages:

- It requires detailed process data. To perform an effective bottleneck accounting analysis, a company must be able to reconstruct the input and output of each stage of its process over a given period. Although many ERP and CRM systems generate this information, smaller companies in particular do not always have access to such data.

- A comprehensive analysis can be cumbersome. Conducting a full bottleneck accounting analysis typically requires specialized software applications or AI-based techniques, which many companies do not have at their disposal.

Bibliography

- Cachon, G., & Terwiesch, C. (2009). Matching supply with demand: An introduction to operations management (2nd ed.). New York: McGraw-Hill.

- Ching, S., Meerkov, S. M., & Zhang, L. (2008). Assembly systems with non-exponential machines: Throughput and bottlenecks. Nonlinear Analysis: Theory, Methods & Applications, 69(3), 911–917.

- Dantzig, G. B. (1965). Linear programming and extensions. Princeton: Princeton University Press.

- Goldratt, E. M., & Cox, J. (1984). The goal: A process of continuous improvement, New York: North River Press.

- Kaplan, R. S. & A. A. Atkinson (1989). Advanced Management Accounting. Prentice-Hall International Inc.

- Krajewski, L. J., Ritzman, L. P., & Malhotra, M. K. (2010). Operations management: Processes and supply chains (9th ed.). New Jersey: Pearson Prentice Hall.

- Lawrence, S. R., & Buss, A. H. (1994). Shifting production bottlenecks: Causes, cures, and conundrums. Production and Operations Management, 3(1), 21–37.

- Li, L., Chang, Q., & Ni, J. (2009). Data driven bottleneck detection of manufacturing systems. International Journal of Production Research, 47(18), 5019–5036.

- Pollett, P. K. (2000). Modelling congestion in closed queueing networks. International Transactions in Operational Research, 7(4–5), 319–330.

- Roser, C., Nakano, M., & Tanaka, M. (2001). A practical bottleneck detection method. In Peters, B. A., Smith, J. S., Medeiros, D. J. & Rohrer, M. W. (eds.), Proceedings of the 2001 Winter Simulation Conference (pp. 949–953). IEEE Computer Society.

- Slack, N., Chambers, S. & Johnston, R. (2010). Operations Management (6th ed.). Essex: Pearson Education.

- Schmenner, R. W., & Swink, M. L. (1998). On theory in operations management. Journal of Operations Management, 17(1), 97–113.

- Veltman, M. (2011). ‘Bottleneck accounting’, Maandblad voor Accountancy en Bedrijfseconomie, pp. 299–305, Juni 2011.

- Veltman, M., Kooij, R. & Marban, S. (2014). ‘Sales Bottlenecks And Their Effect On Profit’, The Journal of Applied Business Research, Vol 30, No 6, pp. 1725–1738, November/December 2014.