Bottleneck Accounting

Summary

Bottleneck accounting is a managerial accounting tool which helps you to determine:

Bottlenecks

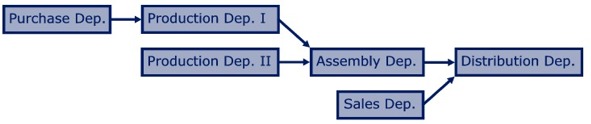

A company usually has several stages involved in the production and selling of

a product or service. For example:

In practice, bottlenecks will usually arise to constrain the amount of

products the firm can deliver (Kaplan and Atkinson, pp. 62). A bottleneck is

the capacity constraining stage governing the output of the entire process

(Slack et al, 2010). Various authors emphasize that in order to improve the output of the total production process

bottlenecks in the production process must be found and managed. Schmenner and Swink (1998) cite the Law of Bottlenecks

that states that the productivity of a production process is improved by eliminating or by better managing its bottlenecks.

The purely practitioner-oriented work of Goldratt (1984) also emphasises that a company must concentrate on its bottlenecks

in the production process in order to improve the overall performance.

Existing bottleneck detection methods

In recent years many methods that can be used to search for bottlenecks have been presented in the literature, for example:

- methods that detect bottlenecks based upon queue length (Lawrence and Buss, 1994 and Pollett, 2000);

- methods that detect bottlenecks based on the maximal production capacity of production factors (Dantzig 1965);

- methods that detect bottlenecks based on the utilization of production factors (Krajewski et al, 2010 and Cachon & Terwiesch, 2009);

- methods that detect bottlenecks based on the active and inactive periods of machines (Roser et al, 2001);

- methods that detect bottlenecks based on the the time a machine is inactive because it is waiting for the arrival of parts, a period called "starvation" or for their removal, a period called "blockage" (Ching et al, 2008 and Li et al, 2009).

The negative effect that a bottleneck has on profit demonstrates the urgent need to eliminate the bottleneck. Therefore, a bottleneck with less impact on profit should be given a lower priority than a bottleneck that has a drastic effect on profit. In order to determine the priority of a bottleneck, a company should determine what effect a bottleneck has on profit. However, the existing methods which detect bottlenecks by measuring queue lengths, active periods, inactive periods, periods of blockage or periods of starvation do not calculate the effect a bottleneck has on profit.

The bottleneck accounting method

Bottleneck accounting is a suitable method to determine bottlenecks and their effect on profit, regardless of the stage

in which these bottlenecks occur. The bottleneck accounting method detects the bottlenecks based on the input and output

of each stage in the total production or service delivery process and the initial inventories of work in progress. It can

therefore analyze all stages of the total process and thus, detect the bottleneck that actually limits sales and profit.

The bottleneck accounting method also calculates the effect a bottleneck has on profit. As a result, the bottleneck accounting method

enables companies to focus on solving the most urgent bottlenecks

(see also see Veltman et al, 2014 ).

The bottleneck accounting method can be used in a variance analysis:

In a traditional variance analysis, managerial accountants analyse the

differences between the sales target and actual sales. Typicaly differences

between targeted sales and actual sales are analysed as below (see also

Horngren and Foster, pp. 138-271).

This report indicates that the actual number of products (volume) sold was

lower than the target number of products (negative volume variance) and the

average sales price of products was lower than the target sales price

(negative price variance). The negative volume variance and the negative

price variance explain the difference between the sales target and actual

sales.

This traditional variance analysis however does not point out which bottleneck(s) caused the negative volume

variance. That is why a traditional variance analysis can't be used to solve

bottlenecks in an organization.

Thus, with traditional accounting techniques you just report that the actual

number of products (volume) sold was lower than the target number of products

(negative volume variance). With bottleneck accounting however you specify

this negative volume variance by showing the bottleneck(s) which caused

this negative volume variance (Veltman, 2011).

An example of a bottleneck accounting report is shown below:

This report indicates which bottlenecks caused a lower

actual sales number: the casting stage and a decline in market demand.

With bottleneck accounting you thus report bottlenecks inside the company

(the casting stage) and bottlenecks outside the company (market demand).

This report also shows the magnitude of each bottleneck. The magnitude of the

bottleneck is the part of targeted sales which is missed as a result of the

existence of the bottleneck. In this case $ 1.114.000 was missed because of

the casting bottleneck, $ 500.000 was missed because of the market demand

bottleneck and another $ 180.000 was missed because of other bottlenecks.

The magnitude of the bottleneck indicates how urgent the bottleneck is. This

case indicates that management should focus on the casting stage first

(for instance by increasing the capacity of the casting stage). Secondly,

management should focus on the market demand (improve the marketing for

instance).

Thus, with bottleneck accounting you not only report which are the

bottlenecks to solve, you also point out which bottlenecks are to be handled

first. In that way bottleneck accounting will make your management more aware

of the necessity to solve bottlenecks and of the correct order in which to

eliminate them.

BIBLIOGRAPHY

- Cachon, G., & Terwiesch, C. (2009). Matching supply with demand: An introduction to operations management (2nd ed.). New York: McGraw-Hill.

- Ching, S., Meerkov, S. M., & Zhang, L. (2008). Assembly systems with non-exponential machines: Throughput and bottlenecks. Nonlinear Analysis: Theory, Methods & Applications, 69(3), 911-917.

- Dantzig, G. B. (1965). Linear programming and extensions. Princeton: Princeton University Press.

- Goldratt, E. M., & Cox, J. (1984). The goal: A process of continuous improvement, New York: North River Press.

- Hillier, F., & Lieberman, G. (2005). Introduction to operations research (8th ed.) New York: McGraw-Hill.

- Horngren, C. T., & Foster, G. (1987). Cost accounting: A managerial emphasis (6th ed.). London: Prentice-Hall International, Inc.

- Kaplan, R.S. & A.A. Atkinson, (1989), Advanced Management Accounting, Prentice-Hall International Inc. 1989.

- Krajewski, L. J., Ritzman, L. P., & Malhotra. M. K. (2010). Operations management: Processes and supply chains (9th ed.). New Jersey: Pearson Prentice Hall.

- Lawrence, S. R., & Buss, A. H. (1994). Shifting production bottlenecks: Causes, cures, and conundrums. Production and Operations Management, 3(1), 21-37.

- Li, L., Chang, Q., & Ni, J. (2009). D.ta driven bottleneck detection of manufacturing systems. International Journal of Production Research, 47(18), 5019-5036.

- Pollett, P. K. (2000). Modelling congestion in closed queueing networks. International Transactions in Operational Research, 7(4-5), 319-330.

- Roser, C., Nakano, M., & Tanaka, M. (2001). A practical bottleneck detection method. Peters, B.A., Smith, J. S., Medeiros, D. J. & Rohrer M. W. eds. in Proceedings of the 2001 Winter Simulation Conference (pp. 949-953). IEEE Computer Society.

- Slack, N., Chambers, S. & Johnston, R.(2010). �Operations Management� (6th ed.) Essex: Pearson Education. 2010.

- Schmenner, R. W., & Swink, M. L. (1998). On theory in operations management. Journal of Operations Management, 17(1), 97-113.

- Veltman, M., (2011).'Bottleneck accounting', Maandblad voor Accountancy en Bedrijfseconomie, pp 299-305, Juni 2011.

- Veltman, M., Kooij, R. & Marban, S., (2014). �Sales Bottlenecks And Their Effect On Profit�, The Journal of Applied Business Research, Vol 30, No 6, pp 1725-1738, November/December 2014.